What If Ireland Defaults? (16 page)

Read What If Ireland Defaults? Online

Authors: Brian Lucey

It seems more likely therefore that an Irish exit from the common currency would have to be unilateral, without any transitional support from the troika. This would be messy and painful for any country. Eurozone exit would result in immediate sovereign and bank default, and bank runs would necessitate capital controls. Ireland would be frozen out of the markets at a time when it is running a primary deficit and needs immediate and ongoing funding for the government to continue offering regular services.

Because of the structure of Ireland's economy, a unilateral Eurozone exit would be particularly disastrous. Ireland's economy during the boom period in the 1990s and especially since the collapse of the property market in 2007â2008 has been heavily reliant on exports as a driver of growth. Ireland's export sector is comprised primarily of multinational corporations (MNCs) that have established their European headquarters in Ireland. The most successful industries, which were relatively resilient even during the depression Ireland experienced in 2008â2010, are the computer services and the pharmachemical goods industries. MNCs are attracted to Ireland for a number of reasons: Ireland boasts a highly educated, English-speaking workforce; the corporate tax rate is only 12.5 per cent and Ireland can offer MNCs rock-solid access to the greater EU market.

This last factor is absolutely key. If Ireland were to unilaterally defy the terms of the EU/IMF bailout agreement and walk away from Eurozone membership it would inevitably raise questions in the minds of MNCs as to Ireland's long-term position in a changing European order. Ireland would risk appearing to be a semi-detached member of a club in turmoil. This is not the ideal foundation on which to build a pitch selling the country as an ideal place to set up shop. Moreover, a unilateral Irish exit would lead to tensions with and resentment from other EU member states, which could manifest itself in a number of ways, including increased pressure to force up Ireland's low rate of corporation tax.

The cost of repaying bank bondholders and official sector loans while undergoing harsh austerity is extremely high. But the cost of unilaterally deciding to exit the Eurozone would undoubtedly be even higher. Ireland would be frozen out of the markets with a primary deficit and without a prayer of getting continued funding from the other EU member states it had just burned. Against this backdrop, the country would then have to develop a new growth model that is less reliant on MNCs for growth. The Irish government would hardly be in a position to provide support for domestic demand, nor would banks be able to offer financing to small, indigenous companies that might fill any vacuum left by MNCs.

Stay the Course

The prospects for the Eurozone staying together are very grim, but this does not necessarily bode poorly for Ireland. Much more important for Ireland than its relationship with the Eurozone is the country's integration in the wider EU market. The repayment of bank and official loans and continued austerity will weigh on Irish public finances and economic growth for years to come. This is indeed a heavy burden that might have been avoided â the Irish government had a number of chances to force a change in the terms of its bailout agreement. Having accepted the bailout terms thus far, however, it is in the country's best interest to continue to comply with the rules set out by the troika. Claims that Ireland's national interest lies in unilaterally leaving the Eurozone are woefully misguided. It is in Ireland's best interest to stay the course and continue to protect its relationship with the EU by maintaining its relationship with the Eurozone.

The Russian Crisis and the Crisis of Russia

Constantin is adjunct professor at the School of Business, Trinity College Dublin, and a director of St Columbanus AG, a Swiss asset management company. An internationally syndicated newspaper columnist, he blogs at

trueeconomics.blogspot.com

.

Introduction

In 1998, following some ten years of structural reforms that began during the late Soviet era under the

perestroika

process and continued after the collapse of the USSR, Russia recorded its first year of economic growth. The nascent middle class, starting to emerge in the country after the tumultuous years of early transition from the Soviet era, was enjoying what appeared to be the second year of rising disposable real incomes.

Then, with virtually no warning, by the end of August 1998, Russia found itself in a financial pariah state position, having defaulted on foreign-held sovereign debt, devalued its currency, imposed strict capital controls and bankrupted a large number of domestic firms and banks. A long-evolving sovereign crisis, having morphed into a fast-moving currency and banking crisis, had left deep scars on the socio-economic environment with middle-class savings either frozen in quasi-solvent banks or destroyed in their totality in dozens of fully insolvent smaller banks and investment funds. Foreign creditors â the lifeblood of an imports-dependent economy â were forced to write down their Russian assets as domestic banks suspended repayments of all external loans.

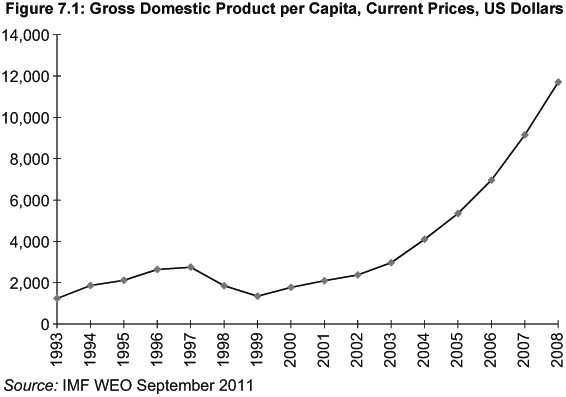

Despite the dramatic disruption caused by the crisis, the Russian economy staged an impressively swift comeback. The pain of the immediate crisis aftermath lasted a relatively brief period of time âapproximately six to eight months â and the economy was able to rebound quickly and sharply. A decade-long economic boom followed the painful adjustments. During this time, the dollar value of Russian economic output increased ten-fold and the stock market rose more than twenty-fold to mid-2008. Devaluation triggered rapid structural rebalancing of the Russian economy and â helped by increases in oil and gas prices and general commodities inflation â by 2000, as shown in Figure 7.1, the economy not only recovered the losses triggered by the default, but also regained all of the ground lost since 1987â1988 reforms.

This process of recovery took a remarkably short period of time, with signs of emergent strengthening of the economy appearing in late 1999 and full macroeconomic recovery firmly established in 2000, less than one and a half years after the default. Russia returned to borrowing from the global markets within twelve months of its default, and booming exports-related revenues, along with prudent fiscal management and reformed tax policies, have resulted in the government repaying most of its debts in full, often ahead of schedule and in some cases even at a premium.

This historically unprecedented experience offers interesting insights and important lessons for the European crisis, and in particular for Ireland, as it highlights the overall importance of growth dynamics in determining the sustainability of a post-default or post-debt restructuring adjustment path. Although in the Russian case growth dynamics were driven by a combination of domestic and foreign factors not open to the Eurozone member states today, from the point of view of the impacted states with strong potential growth fundamentals, such as Ireland, the lessons from the Russian default present a hope for some significant upside potential for swiftly resolving debt overhang problems via a structured default. The Russian experience, however, also shows the importance of tangible and deep reforms in underwriting the process of recovery from the default.

In this context, let us first examine Russia's road to default, and take a brief look at the adjustment and recovery path taken since 1999 through 2008.

The Roots of the Crisis: 1995â1997

The roots of the 1998 Russian crisis can be found in the events that start with the collapse of the USSR, when the Russian economy inherited all of the USSR's debts and crumbling economic institutions and structures. This little known fact, often omitted from the discussion of the role of Russia in the post-Communist economic transition in the broader Central and Eastern Europe and Commonwealth of Independent States (CIS) regions, nonetheless serves as the departure point for the analysis of Russia's fiscal policy dynamics in the 1990s.

In April 1996, Russia began a series of international negotiations aimed at rescheduling the repayment of foreign debts inherited from the USSR. Until then, the Russian economy was saddled with the massive burden of covering $100 billion of debt that it assumed following the collapse of the Soviet Union. Overall, upon dissolution of the USSR, Russia assumed the entire foreign external debt of the Soviet Union despite the fact that Russia accounted for less than half of the total population of the USSR and for approximately 50 per cent of its national income. The level of debt carried by Russia from the USSR was equivalent to 117 per cent of the country's gross domestic product (GDP) in 1992. According to Nadmitov:

1

This level of debt was too heavy for a transitional Russian economy that needed further financial injections [in order to finance investment and transition]. The combination of a fall in output coupled with the fiscal costs associated with the transition made the scheduled debt service a significant burden. For ten years between 1991 and 2001 Russia reached six multilateral debt rescheduling agreements with official creditors, [and] held five formal debt relief and principal deferment negotiations with commercial creditors â¦.

Thus, from the Russian perspective, the 1996 re-negotiations of sovereign debt were a major move in the direction of stabilising the economy.

At the same time, late 1995 and 1996 were marked by improvements in the trade balance. Although the rate of growth in exports of goods and services declined slightly from 7.7 per cent in 1995 to 6.8 per cent in 1996, both years posted well above average increases in export volumes for the entire post-USSR period. At the same time, the rate of growth in imports of goods and services had fallen from 17.7 per cent in 1995 to 6.2 per cent in 1996, marking the first year since the transition began when the growth in exports was exceeding the growth in imports. At the same time, exports of oil rose from $14.6 billion in 1994 to $18.3 billion in 1995 and $23.4 billion in 1996. The heavy dependency of Russia on imports was itself the legacy of the Soviet Union economic organisation, which favoured specialisation across individual republics and between the member states of the COMECON (the common trade area of the former Warsaw Pact) block. Restructuring of this specialisation was always envisioned as a painful and long-term process, which was further disrupted by the mismanagement of trade flows upon the dissolution of the USSR.

Russian GDP in nominal terms rose from $276.9 billion in 1994 to $313.5 billion in 1995 and $391.8 billion in 1996. With slowing inflation (down from 215 per cent in 1994 to 21 per cent in 1996), real economic growth improved from -12.7 per cent in 1994 to -3.6 per cent in 1996. 1997 became the first year in the post-Soviet period when Russian real GDP actually expanded, achieving 1.38 per cent growth year on year. Inflation came under much stricter control at 11 per cent and by the end of 1997 Russian nominal GDP rose to $405 billion.

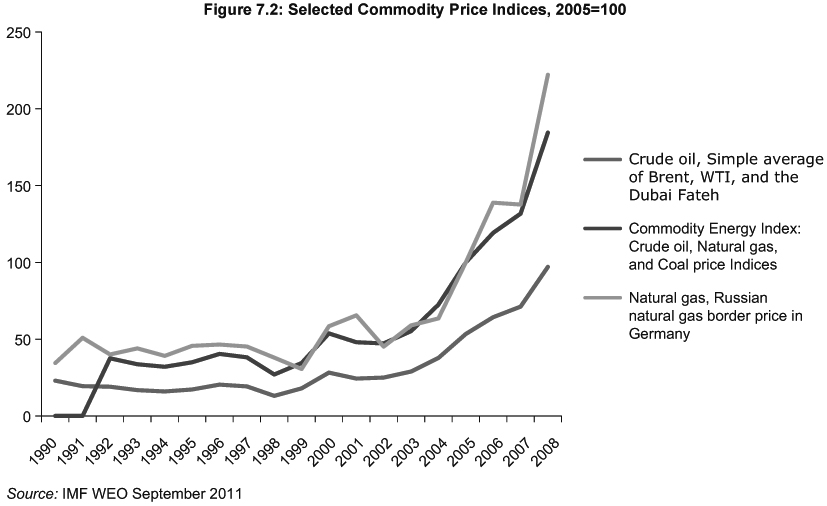

To a large extent, this effect was driven by improved volumes of exports of energy (oil and gas) and other primary materials. As illustrated in Figure 7.2 (index of prices for natural gas), Russian deliveries to Europe firmed up from 39.1 in 1994 to 46.5 in 1996 â the highest level since 1991. Average crude oil prices, which had stood at $15.95 per barrel in 1994, rose to $20.37 per barrel in 1996, also the highest price achieved in five years. Wheat, barley and cereal prices also posted decade highs in terms of prices in 1996, as did tin and nickel. Although energy accounted for 45 per cent of Russian exports by 1997, the overall exports of goods and services were on an improving trend in 1994â1996 and through the first half of 1997. While the legacy debt of the USSR was now close to the sustainable levels, the financing costs required to maintain the government debt remained high.

Russia entered the April 1996 negotiations on debt reduction with the Paris and London Clubs of borrowers â two international arrangements representing large groups of sovereign and private lenders â with its economic performance finally starting to show some signs of life after six years of rapid decline. These transitional years followed two decades of Soviet-era stagnation and economic decay. The analysts' consensus on the Russian economy and fiscal conditions between 1996 and 1997 was, thus, favourable. This change in the outlook was a marked departure from the preceding decades. At the conclusion of these debt talks in September 1997 Russia agreed rescheduling the repayment of some $60 billion worth of ex-Soviet debt with the Paris Club. In October 1997, Russia rescheduled repayments on $33 billion of debts to the London Club. As a part of these agreements, Russia lifted the restrictions on foreign holdings of its sovereign bonds. By the end of 1997, foreign residents held almost one third of all state-issued short-term bills (GKOs).

The Blow Up: 1997â1998

Improved international ratings and subsequent gains in access to international lending markets, however, were not reflected in a matching improvement in the federal government's fiscal performance. Tax collection remained endemically mired in corruption, and harmful regional and federal competition; and the black markets continued to expand.

In addition, based on improving credit ratings, Russian banks aggressively courted foreign funding, with the ratio of foreign liabilities to assets rising from 7 per cent in 1994 to 17 per cent by the end of 1997. Exacerbating this growing risk exposure, the majority of investment contracts held by foreign investors in Russian banks (some $6 billion in total) were short term and held off balance sheet.

This meant that while on the surface the Russian economy was at the starting line for economic recovery, by late 1997/early 1998 a number of structural weaknesses were present behind the scenes. Improved access to external funding coincided with continued declines in private investment: between 1994 and 1997 total investment in Russian economy dropped from 26 per cent to 22 per cent of GDP. Increases in official and banks inflows masked even more pronounced declines in private foreign direct investment (FDI). In addition to endemic tax collection problems, rising unemployment (up to 10.8 per cent in 1997 from 7.2 per cent in 1994) contributed to shortfalls in government revenues. By the end of 1998 general government net borrowing was running at 8 per cent of GDP, the structural deficit widened in 1997 to a massive 16.3 per cent of GDP, and general government debt was on track to hit 100 per cent of GDP in 1997â1998. Wages backlogs exceeded 40 per cent of payrolls by 1997 and tax evasion, including by ordinary workers, was rampant.

Much of the economy remained captured by extraction sectors, with imports of goods rising 11.6 per cent year on year in 1997, while exports of goods were shrinking 1.05 per cent. Agriculture and food, and consumer goods remained particularly weak domestic sectors. By 1997, virtually every shelf in the average Russian supermarket was occupied by imported foodstuffs. Where domestic producers attempted to compete with branded foreign consumer goods, this competition almost invariably took place at the lower end of the value-added spectrum.

The lack of diversification in the Russian economy was caused by a combination of two factors. Firstly, the break-up of the Soviet Union and, equally importantly, the COMECON trading block exposed the Russian economy to a simultaneous loss of some markets for its output and a tightening of supply of consumer goods. Russia's energy, chemicals and heavy industry specialisation within the USSR has led to a de facto de-diversification of its economic activities. There were significant supply disruptions to Russian industry from the former COMECON member states, in effect shutting down production of internationally marketable heavy industrial equipment, aircraft and other goods traditionally specialised in by the Russian economy. Secondly, Russia's development since its 1991 independence from the USSR saw an increasing domestic and foreign capital push toward investment in oil and gas, as well as other extraction industries. Much of the economic policy at federal level reflected this development, especially since tax competition between federal authorities and local governments in the area of corporate tax revenues left the federal state budget more exposed to dependency on exports revenues from oil and gas sales. This further incentivised significant policy biases in favour of extraction sectors between 1993 and 1997.